What is a Broker Credit Score?

A broker credit score measures a freight broker's payment reliability toward carriers. It factors in average days to pay, payment history, bond status, complaint volume, and authority age — giving carriers a data-driven way to decide whether a broker is safe to haul for. Checking a broker's credit score before accepting a load is one of the most important steps a carrier or owner-operator can take to protect their cash flow.

Key Takeaways

- A broker credit score rates a freight broker's payment reliability toward carriers, similar to a personal credit score but focused on whether the broker pays trucking companies.

- Scores are compiled by third-party platforms — Carrier411 (1-5 stars), TransCredit (1-100 scale), and Highway (letter grades A-F) — using carrier-reported payment data.

- Days to pay (DTP) is the most important metric: under 30 days is good, under 21 is excellent, and 46+ days is a red flag for likely non-payment.

- Every broker must maintain a $75,000 surety bond (BMC-84), but it rarely covers all carrier claims when a broker fails, so prevention beats recovery.

- Checking a broker's credit takes about two minutes and costs nothing on FMCSA SAFER up to roughly $35/month on Carrier411 — far cheaper than an unpaid load.

- A broker with no credit history is not automatically bad but carries higher risk; many carriers avoid brokers with under 6 months of authority and few payment reports.

Ahmad Qazi

Founder & CEO, O Trucking LLC

Fact-Checked by O Trucking Dispatch Team

5+ years dispatching for carriers, verifying broker credit scores, and managing broker payment risk on every load

Written by Ahmad Qazi, founder of O Trucking LLC, drawing on 9+ years dispatching for owner-operators. Learn more about us.

What Is a Broker Credit Score?

A broker credit score is a numerical or letter-grade rating assigned to a freight broker based on their payment history with carriers. Think of it like a personal credit score, but instead of measuring how you pay your credit card company, it measures how reliably a broker pays the trucking companies that haul their freight.

These scores are compiled by third-party platforms — primarily Carrier411, Highway (formerly Truckstop Credit), and TransCredit — using payment data reported by carriers, factoring companies, and public records from FMCSA. The data typically includes:

- Days to pay (DTP) — average calendar days from delivery to carrier payment

- Payment history — number of on-time payments vs late or missed payments

- Bond status — whether the broker's $75,000 surety bond (BMC-84) is active

- Complaint volume — number of carrier complaints filed with FMCSA

- Authority age — how long the broker has held active authority

- Bond claims — whether carriers have filed claims against the broker's surety bond

- Double-brokering reports — any history of illegally re-brokering loads

No single data point tells the full story. A broker might have a high days-to-pay average but zero complaints — meaning they pay slowly but always pay. Another broker might have fast payment on most loads but multiple bond claims, suggesting selective non-payment. The credit score aggregates all of these signals into a single assessment that helps carriers make faster decisions.

Credit Score Scales by Platform

Carrier411

1-5 stars based on carrier payment reports. 4-5 stars = reliable.

TransCredit

1-100 scale. 75+ is good, 90+ is excellent.

Highway

Letter grades (A-F). A and B grades = reliable payers.

Why Broker Credit Scores Matter

Non-payment and slow payment by brokers is one of the biggest financial risks facing carriers and owner-operators. When a broker does not pay, the carrier has already burned fuel, paid the driver, and worn out the truck — all costs that cannot be recovered. A single unpaid load can wipe out an entire week's profit for a small carrier.

The broker's surety bond is only $75,000 — a small amount that can be exhausted quickly if multiple carriers file claims simultaneously. If a broker owes $200,000 across 10 carriers and the bond is only $75,000, carriers will receive pennies on the dollar. The bond is a last resort, not a guarantee of full payment.

Checking a broker's credit score takes about two minutes and costs nothing (FMCSA SAFER) to $35 per month (Carrier411). Compare that to the cost of hauling a $2,000 load and never getting paid. Every carrier should make broker credit checks a non-negotiable part of their load-acceptance process.

The $75K Bond Is Not Enough to Cover Large Losses

How to Check a Broker's Credit Score

Checking a broker's credit should be a standard step before accepting any load. Here is the process most experienced carriers and dispatchers follow:

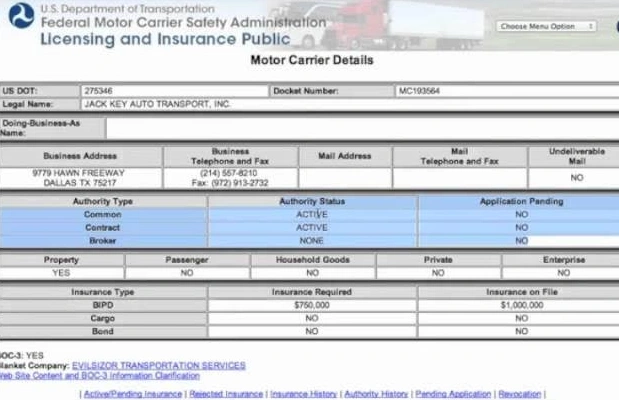

Verify Authority on FMCSA SAFER (Free)

Go to safer.fmcsa.dot.gov and look up the broker by MC number or company name. Confirm their broker authority is “Active” and their surety bond (BMC-84) is on file. If the authority is not active or the bond is missing, stop — do not haul for this broker under any circumstances.

Check Days to Pay and Credit Score (Paid)

Use Carrier411, Highway, or TransCredit to pull the broker's credit score and average days to pay. Look for a DTP under 30 days and a score that indicates reliable payment. Cross-reference across multiple platforms if possible — each has different data sources and may show different results.

Read Carrier Reviews and Comments

Numbers tell part of the story, but carrier comments fill in the gaps. Read what other carriers have reported about their experience with this broker. Look for patterns — one negative review might be a disgruntled carrier, but multiple complaints about the same issue (slow pay, deductions, refusal to pay accessorials) is a red flag.

Check FMCSA Complaint History

Search the broker's MC number at nccdb.fmcsa.dot.gov to see if carriers have filed formal complaints. FMCSA complaints are public record and indicate serious payment disputes — not just minor disagreements.

For a detailed walkthrough with screenshots and tips on each platform, see our step-by-step guide to checking broker credit scores.

Check Credit Before You Negotiate, Not After

Best Broker Credit Check Tools

Several platforms provide broker credit data, each with different strengths. Here is a quick comparison:

| Tool | Cost | Key Features | Best For |

|---|---|---|---|

| Carrier411 | $34.95/mo | Carrier reviews, DTP data, star ratings, double-brokering alerts | Most carriers |

| Highway | Free / Paid | Letter grades, carrier community data, load board integration | Budget-conscious |

| TransCredit | Per report | 1-100 score, factoring company data, detailed payment history | Factored carriers |

| FMCSA SAFER | Free | Authority status, bond status, complaint history, basic info | Quick verification |

| Chameleon | Varies | TMS-integrated credit checks, automated monitoring | Dispatch services |

Most experienced carriers use a combination of FMCSA SAFER (free, for authority verification) plus one paid platform for credit scores and payment data. Carrier411 is the most widely used in the owner-operator community, while TransCredit is popular with carriers that use factoring companies. For a detailed comparison with pricing and features, see our best broker credit check tools guide.

Days to Pay Explained

Days to pay (DTP) is the single most important metric in a broker's credit profile. It measures the average number of calendar days between when a carrier delivers a load and when the broker sends payment. Here is how to interpret DTP numbers:

| Days to Pay | Rating | What It Means |

|---|---|---|

| 1-7 days | Excellent | Quick pay or immediate payment. Uncommon unless the broker offers QuickPay. |

| 8-21 days | Very Good | Faster than industry average. Broker values carrier relationships. |

| 22-30 days | Standard | Industry norm (Net 30). Most brokers fall in this range. |

| 31-45 days | Slow | Slower than average. May indicate cash flow issues. Proceed with caution. |

| 46+ days | Red Flag | Significantly late. High risk of non-payment. Avoid unless you have a very good reason. |

Keep in mind that DTP averages can be skewed. A broker with a 28-day average might pay most carriers in 15 days but have a few outlier payments at 60+ days that pull the average up. Always read the individual payment reports in addition to the average. For a deeper dive, see our broker days to pay explained guide.

QuickPay Changes the DTP Calculation

Broker Credit Score Red Flags

Beyond the credit score number itself, there are specific warning signs that a broker may not pay. Any single red flag warrants caution; multiple red flags should be a dealbreaker:

New authority (under 6 months) — New brokers have no track record. While many are legitimate, the highest rates of non-payment come from newly licensed brokers who disappear after collecting shipper payments.

No surety bond on file — Every broker must maintain a $75,000 surety bond (BMC-84) filed with FMCSA. If the bond is not showing as active on SAFER, the broker is operating illegally.

Days to pay over 45 — Consistently late payment indicates cash flow problems. The broker may be using your payment to cover other obligations.

Multiple FMCSA complaints — A few complaints on a large broker are normal. But a high complaint-to-load ratio, especially recent complaints, signals a pattern of non-payment.

Double-brokering history — If a broker has been reported for double-brokering, it means they re-brokered loads they were supposed to arrange directly — a deceptive and often illegal practice.

Rates significantly above market — If a broker is offering rates 30-40% above market, ask yourself why no one else took the load. Scam brokers use above-market rates to lure carriers, then disappear after delivery.

Unverifiable physical address — Legitimate brokers have real office addresses. If the address on SAFER leads to a UPS Store, a virtual office, or a vacant lot, proceed with extreme caution.

For a comprehensive breakdown of every red flag and what to do when you spot them, see our broker credit score red flags guide.

How to Protect Yourself from Non-Paying Brokers

Checking credit scores is the first line of defense, but it is not the only step. Here is a comprehensive protection strategy:

Check credit on every load — Not just new brokers. Established brokers can develop payment problems too. Make it part of your standard booking process.

Get a signed rate confirmation before loading — Never haul without a signed rate con that specifies the rate, payment terms, and broker information. This is your legal proof of the agreement.

Verify the MC number on the rate con matches SAFER — Scam brokers sometimes use the MC number of a legitimate broker. Call the broker directly using the phone number from SAFER (not the rate con) to confirm the load is real.

Use a factoring company — Factoring transfers payment risk from you to the factor. The factor pays you immediately (minus a fee) and collects from the broker. Most factors check broker credit before approving invoices.

Submit proof of delivery immediately — Submit your signed BOL and POD the same day you deliver. The clock on payment terms does not start until the broker has your paperwork. Delays in paperwork submission mean delays in payment.

Know the bond claim process — If a broker does not pay, you can file a claim against their $75,000 surety bond. You have 18 months from the delivery date to file. For the step-by-step process, see our broker bond claims guide.

Report Every Payment Experience — Good and Bad

How Our Dispatch Team Verifies Brokers

Broker credit verification is built into every load our dispatch team books. At O Trucking LLC, we do not let carriers haul for brokers we have not vetted:

Credit check on every broker, every load

Before we book any load, we verify the broker's authority status on SAFER, check their credit score and days-to-pay data on Carrier411, and review recent carrier payment reports. Brokers that fail our credit screen do not get booked — period. This protects our carriers from payment risk before they ever pick up a load.

Double-brokering detection

We verify that the broker posting the load is the broker on the rate confirmation. We cross-reference MC numbers, check for double-brokering reports, and call the broker directly using the SAFER phone number to confirm load details. This catches double-brokered loads before our carriers are exposed to them.

Payment tracking and follow-up

We track payment status on every load and follow up with brokers who are approaching their payment deadline. If a broker is late, we escalate through their accounting department before it becomes a collections issue. Our carriers get paid on time because we do not let invoices fall through the cracks.

Related Resources

Freight Broker

What brokers do and how they operate

How to Verify Freight Brokers

Complete broker verification process

How to Check Broker Credit

Step-by-step credit check guide

Double Brokering Protection

Detect and prevent double-brokered loads

How to Report a Bad Broker

File complaints, bond claims, and reports

Broker Payment Terms

Net 30, QuickPay, and payment structures

Broker Credit Score FAQ

Common questions about broker credit scores, payment verification, and protecting your trucking business

What is a broker credit score in trucking?

A broker credit score is a numerical rating that measures how reliably a freight broker pays carriers. It aggregates data on average days to pay, payment history, bond claim filings, complaint volume, and authority age. Platforms like Carrier411, Highway (formerly Truckstop Credit), and TransCredit each calculate their own proprietary scores. Carriers use these scores to decide whether to accept loads from a particular broker — a low credit score means higher risk of slow payment, short payment, or no payment at all.

How do I check a freight broker's credit score for free?

You can check basic broker information for free on the FMCSA SAFER System (safer.fmcsa.dot.gov), which shows authority status, insurance filings, bond status, and complaint history. However, SAFER does not provide a credit score or days-to-pay data. For actual credit scores and payment history, you need a paid service like Carrier411 ($34.95/month), Highway (free basic tier with limited data), or TransCredit (per-report pricing). Some factoring companies also provide broker credit checks to their clients at no extra charge.

What is a good broker credit score?

It depends on the platform. On Carrier411, brokers are rated from 1 to 5 stars based on carrier reports — 4 to 5 stars indicates a reliable payer. TransCredit uses a 1 to 100 scale where 75+ is considered good and 90+ is excellent. Highway uses a letter-grade system where A and B grades indicate reliable payment. Regardless of the platform, the key numbers to focus on are days to pay (under 30 is good, under 21 is excellent) and complaint volume (zero is ideal, but a few resolved complaints on an established broker are normal).

What does 'days to pay' mean for a freight broker?

Days to pay (DTP) is the average number of calendar days it takes a broker to pay a carrier after delivery. The industry standard is 30 days (Net 30). A DTP under 21 days is considered excellent, 22-30 is standard, 31-45 is slow but common, and anything over 45 days is a red flag. Some brokers offer QuickPay programs that pay in 1-5 days for a fee (typically 1-5% of the load). Days-to-pay data is collected from carrier payment reports and is available through Carrier411, Highway, and TransCredit.

Can I report a broker who didn't pay me?

Yes. You can report non-paying brokers through multiple channels: (1) file a complaint with FMCSA at nccdb.fmcsa.dot.gov, (2) post a payment report on Carrier411 or Highway, (3) file a bond claim against the broker's $75,000 surety bond (BMC-84), and (4) file a complaint with your state's attorney general. Filing a bond claim is the most direct path to recovering money — the surety company must investigate and respond within 60 days. See our how to report a bad broker guide for the full process.

Should I always check a broker's credit score before accepting a load?

Yes. Checking a broker's credit score before accepting a load is one of the most important risk management steps a carrier can take. A 2-minute credit check can prevent months of chasing unpaid invoices or filing bond claims. At minimum, verify the broker's authority is active on FMCSA SAFER and check their days-to-pay data on Carrier411 or Highway. If you are using a dispatch service, your dispatcher should be doing this verification on every load before booking.

What happens if a broker has no credit score or payment history?

A broker with no credit history is not necessarily a bad broker — they may be newly licensed. However, a new broker with no track record carries inherently higher risk. If you decide to haul for a new broker, take extra precautions: verify their surety bond is active, get the rate confirmation signed before loading, confirm their physical address is real, ask for QuickPay or payment at delivery, and consider requiring partial payment upfront. Many experienced carriers avoid brokers with less than 6 months of authority and fewer than 10 payment reports.

Need a Dispatch Team That Vets Every Broker?

Our dispatchers check broker credit scores, verify authority, and screen for red flags on every single load before booking. We protect our carriers from non-paying brokers so you can focus on driving.